Many people feel a pull to renew their life and make big changes around the new year, with New Year’s Eve being the calendar point that makes people feel THIS year can be completely different than the last.

Once you’ve begun to improve your financial confidence, everything else in life begins to improve > not only can you plan for your income and save for necessities and lifesyle improvements, having less financial stress in your everyday life can open up stores of mental and emotional energy that was being sucked into managing stress, now you can reclaim and apply in more productive ways like self care, including reconnecting with friends and family and your community.

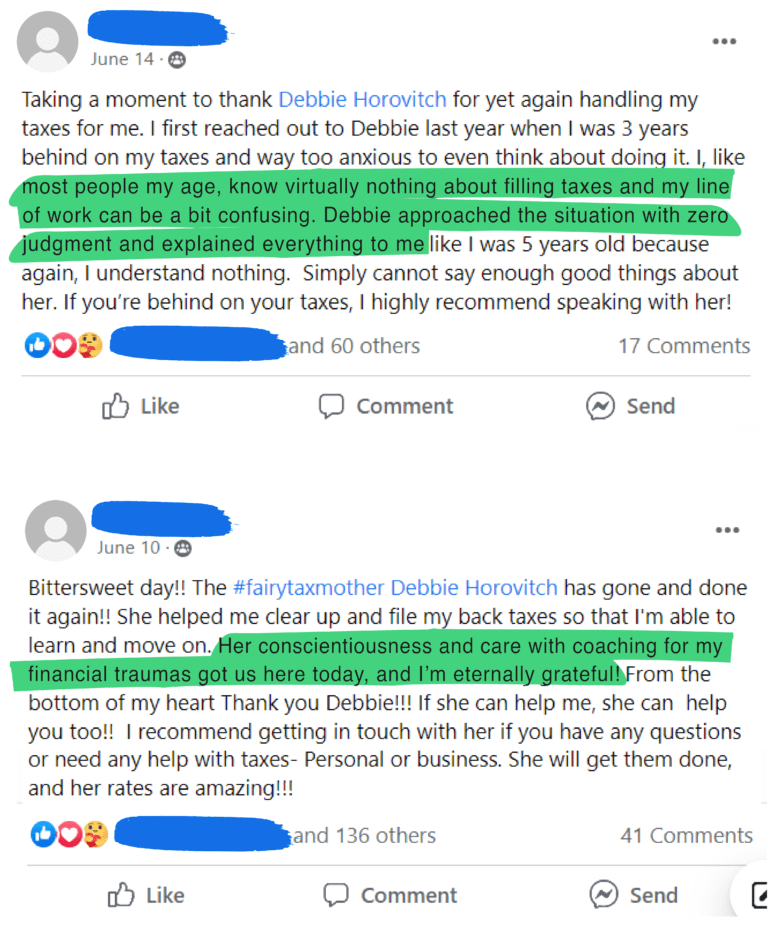

Every year I’m surprised when new clients reach out to me for help filing multiple years of taxes in the first week of January and even sometimes literally on January 1st. The stress of years of ongoing fear of ramifications of filing, and the amounts of taxes and penalties/fines that could be due, gets to a point that it HAS TO STOP, and they come to me for relief. Catching up on back taxes is a great step, but it’s temporary and limited in it’s benefit to your life right away.

If you want to make this next year the most powerful year of financial changes in your life: changing how you feel and think about money, spending, and saving, so that you can evolve dramatically towards financial confidence – this article will provide you with a plan. A few simple steps that will continuously benefit you, for as long as you apply them.

To be able to make any major change in your life, especially money, you’ll need to change your habits, beliefs, and thinking.

Starting backwards (with thinking) comes from planning the end results that you want, and considering all the ways you could use to get yourself there. Or looking at it another way, think about what you would need to change about yourself, to make it easier and more likely to get you successfully to your end goal.

Change Your Money Thinking & Habits

Throughout history the belief that you should “pay yourself first” has always prevailed as the strongest recommendation for personal financial empowerment, but in this day & age, with all the tech distractions available, it’s hard to remember and think about actually transferring money to savings. To help combat this, Michalowicz’s Profit First system recommends automating the savings activity, so that all you have to do (if you want to) is check your bank account to see your savings accounts growing – a regular habit that we all probably do quite often.

Profit First recommends setting up the most important account, the dedicated savings account for your profits FIRST, with an automatic savings rule of 1%-3% for owner’s profit. This is not the owner’s regular pay, or performance bonuses, this is the additional PROFIT payment owners get, as the reward for building a business, managing clients & systems, and employing other people. Without a separate savings account for profits (and also one for tax savings), most entrepreneurs fall perpetually into annual losses with their business spending all or even more of the revenue earned.

Even if you’re not self-employed, you can still consider yourself the “business owner” of your life, with a goal to live a profitable life, where you create and give a lot of value, and that is what allows you to still keep a surprising amount for yourself. Another well-known classic book The Richest Man in Babylon, by George S. Clason also suggests always setting aside, and then INVESTING 10% of your earnings. So depending on your situation, try setting an automation rule on your account to save up to 10% long term, and 10% for short term / emergency savings. I know 20% can seem like “too much!” but it will cost you nothing to simply move the money back into your chequeing account if you need it, and you’ll always be happy to have whatever is left in your savings account.

When I first started the Profit First system, it felt like I was spending everything (my impulse) I had, because my main account was often empty or nearly empty. I could see the automated savings transactions happening everyday, anytime I checked my account – which prevented me from spending unconsciously, and I was astounded at the speed of how quickly my savings grew to levels I have NEVER enjoyed before.

To encourage savings growth & then investment, start “shopping for your future” by educating yourself (for free) in an area of investing that you want to learn about, so you can be ready for when you have the money to invest. I’ve been looking at properties in a small town in Mississippi, and even got to the point earlier this year (within months of implementing these rules on my accounts) where I had as much in my bank accounts, as the price of an extremely low-priced, reno-needing property I was watching on Zillow. That BLEW. MY. MIND. I didn’t buy it, but it gave me the encouragement that I can buy a home someday soon, something I had never considered was realistic, until that day.

Especially when self-employed it’s common to find dips in earnings that mean suddenly you feel back at square one with all your accounts empty again, so to prevent using your emergency savings too soon or too often, try to reduce your spending.

Reduce Your Spending

The most accessible and immediate way to increase the amount of money you have available for specific goals is to reduce your spending.

On a quarterly basis, spend an afternoon focused on reducing all unnecessary spending:

★ Pause or Cancel: Review all your monthly subscriptions to temporarily “pause” charges or cancel the account all together. Do this for BOTH personal AND business spending.

★ Develop a habit ofWAITING to spend money. Mike Michalowicz recommends developing a regular challenge that everytime you’re going to buy anything new, you WAIT ONE MORE DAY to buy it, if you possibly can. Scarcity used in sales is an effective tactic to get you to commit earlier; but once you’ve bought there are MANY reasons why it’s often impossible or difficult for you to ever get the value you’d hoped from the purchase or even your money back.

★ Substitutions & Replacements: Instead of buying bottles of wine at the restaurant, bring wine with you or host a dinner party. Instead of buying a coffee and bagel every morning, bring it from home & drink coffee at the office for free. Instead of feeling like you NEED to have your hair professionally cut & coloured regularly, can you adjust your brand to allow for your natural grey hair to grow out? I was able to finally break my personal persistent need for perfectly chocolate brown hair, with a smart cut for social media consulting (youthful expert brand), and “rebrand” for a new career in classic accounting/taxes and became the Tax Fairy Godmother, where more experience and a matronly presence is valued. It helps my business, reduces chemical stress in my life, and saves me hundreds of dollars per year.

Each time you go through a series of spending cuts, total the amount of monthly and annual saved spending, and make a specific plan to reallocate that money intentionally to another more valuable purposein your life.

The more obvious way to increase the amount of money you have to fund specific goals, is to increase your earnings.

Increase Your Income With a Side-Hustle

Fundamentally, increasing your income is just a matter of increasing the value you give out to other individuals & organizations, which they pay you for.

With employment, in theory, anyone should be able to get a job, which will earn them income. The lower-paying the job, generally, the less specific skills are needed to do the job well. Regardless of how well you do your job, you’ll almost always be rewarded financially, but you’re still going to be limited by your employer’s expectations, availability, and need for what you have to offer. Your efforts are usually compensated the same/similar amount of pay, at the scheduled pay periods, regardless of how well you do the job.

With self-employment, you’re always the most in control person of your business, and even though you might not always be compensated immediately for every action you take, you CAN enjoy eventual value for every experience in self-employment, whether it’s a financial success or simply a way of improving the value you have to offer future opportunities

The best and least risky way to start self-employment is as a “hobby” or area of life that you’re passionate about already. Whatever you like to do to pass your leisure time, to connect with your community, or to improve your lifestyle, is something that you can use to decide to offer help to other people in the community around that activity. Whatever you can do better than people who are just starting out, is something that you can do to offer help that is of value.

Start your side-hustle simply! No need for upfront spending on branding, advance business registrations, coaching or otherwise… Just start by finding ways to collect money from customers, in exchange for a product or service that helps them get to the level that you’re already at or beyond.

Once your side-hustle is earning money, then you can decide to reinvest in expenses to attempt to grow, or you can choose to take the profits out of your business (keeping it small) to use in other personal ways.

This could be a longer road to continuously increase your earnings, as you’ll have to discover & develop the VALUE you will be offering, in order to get clients’ payments, and to balance it with the demands of your job and personal life; but starting a side-hustle will ALWAYS pay you back for your investments eventually, unlike simply asking your employer for a raise or finding another job, which will only pay you for your time/effort put in for your employer.

File Your Back Taxes

If you haven’t yet filed your taxes for the previous year, or for many years past, there is a great potential financial opportunity in getting caught up on your tax filing.

If you owe money to the CRA for previous years’ tax returns, then getting caught up on filing will immediately cease the most significant financial penalties (10% of the amount due, and then 1% or 2% monthly for 10 or 20 months until you file returns). Even if you’re unable to make payments at all currently, it will help you enormously to stop late-filing penalties on any years that you might not have filed.

If you’re late to file and owed a refund amount from last year or multiple years, great! Getting the money (that you earned previously) back into your accounts early, allows you to control it. In my experience, the majority of my clients who are multiple years behind, are the most likely to be receiving refund amounts overall from catching up, even when some years might owe, its unusual for there to be a balance overall, unless they’re mostly self-employed returns.

Additionally, if you’ve been struggling to get ahead financially and you’ve been lower-income, then you’re likely to qualify for additional low-income taxpayer benefits that are calculated based on your annual tax return details. The most common benefits people with lower income can receive are: Climate Action Incentive, GST Credit, Trillium Benefits, and Canada Child Benefits, but there are many others that you could qualify to receive, determined only by filing your income tax returns.

If ADHD or anxiety has kept you overwhelmed from filing your taxes this year, or many years previous, I can help. Before becoming Canada’s Tax Fairy Godmother I was 10 years behind on filing my self-employed T1 tax returns and running away from all the CRA’s attempts to get me to file, and catch up. I was riddled with imposter syndrome and fear of success due to my financial situation being such a mess, and it took the CRA threatening legal action against me for me to finally decide I was DONE with being functionally financially illiterate and would do whatever I needed to do to finally embrace financial responsibilities in my life, for myself.

Although the last few years have been unprecedented for everyone, these 4 steps have helped me stabilise my income and spending, and create a habit of savings that truly feels good. I can’t wait to see how it helps me through the coming years, and would love to hear how it helps you too.

Tax Fairy Godmother

Debbie Horovitch