Holding foreign property in the tax year with a total cost over $100,000 must be reported on form T1135, due on the same date as your tax return is due.

The penalties for late reporting are $25/day, up to $2500 max.

Includes

– funds or intangible property (patents, copyrights, etc.) situated, deposited or held outside Canada

– tangible property situated outside Canada

– a share of the capital stock of a non-resident corporation

– shares of corporations resident in Canada held outside Canada

– an interest in a non-resident trust that was acquired for consideration

– an interest in a partnership that holds a specified foreign property unless the partnership is required to file Form T1135

– a property that is convertible into, exchangeable for, or confers a right to acquire a property that is specified foreign property

– a debt owed by a non-resident, including government and corporate bonds, debentures, mortgages, and notes receivable

– an interest in a foreign insurance policy

– precious metals, gold certificates, and futures contracts held outside Canada

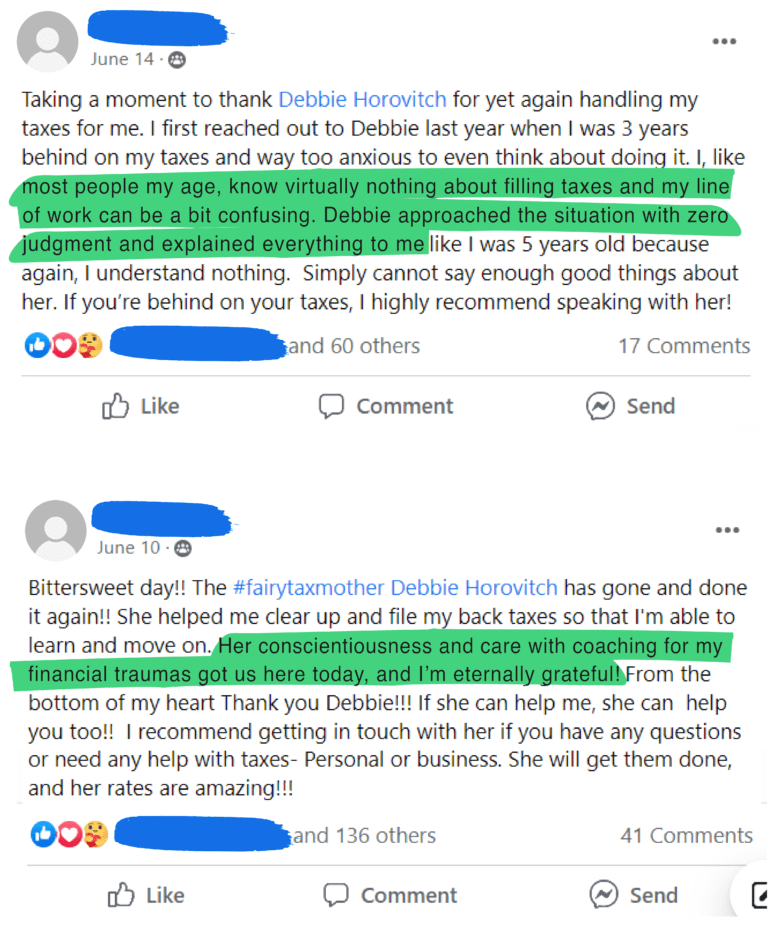

Tax Fairy Godmother

Debbie Horovitch